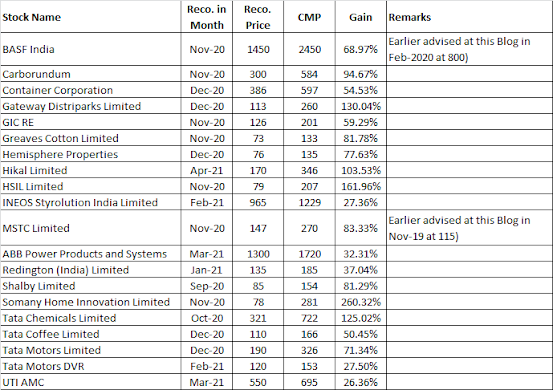

Grade: TIER 1

(This business study of Tata coffee Ltd is taken from the Monthly Newsletter (Jan-21 Edition) of this Blog. The sample of Jan-21 edition was shared at this blog on 28th Jan, 2021.)

Coffee: A

global Drink

1) Coffee truly is a global drink

and a global commodity. However there are disputes related to this being second

most traded commodity after oil. Many argue that this is not the case as agro

commodities like Wheat or rice are having much bigger trade value. But I think,

Coffee may be a big trade commodity if we take into account only the

international trades as other agro commodities like wheat or rice are mostly

traded in the production country and international trade may be much lower than

the total production. Even on standalone basis the value of international trade

(exports) is significant at USD 30 billion.

Coffee generally is of two

types-Arabica and Robusta. Arabica is of premium quality with half of caffeine

levels as compared to Robusta. So it has much deeper, smoother and sweeter

taste with notes of chocolate and hints of other fruits flavor. So Arabica has

much higher and intense flavors. Robusta is much stronger in taste with almost

twice the caffeine levels. So due to higher caffeine levels, it is much bitter

and harsher in taste with notes of grains. Robusta is much easier to cultivate,

has almost double the yield and less prone to insect attacks (due to high

caffeine) so all these factors makes it to cost lower. But Arabica beans are

sold at double the price. The instant powdered coffee we find in all the retail

stores is all robusta coffee. In order to drive up the profits, producers are

using more and more of robusta coffee whether it is instant coffee or a coffee

retail chain.

Across the globe, Arabica

accounts for some 75% production share while Robusta is 25% share. Brazil leads

the globe with Arabica production (70% of its total coffee production) while

Vietnam is the leader in Robusta (95% of its total coffee production). The

global coffee production data is as follows:

2) Europe accounts for some 35%

consumption with nil production. Europe and North/South America account for

some 65% of total global coffee consumption. Europe and USA are fairly stable

in coffee demand so now it is India and China which are the new coffee hot

spots. India’s coffee consumption is concentrated to southern India but off

late with the growth in coffee retail chains like CCD and Starbucks a strong

coffee culture is happening in India which is going to enter their houses also.

With the availability of premium coffee beans and electric roasters and coffee

makers the home consumption is going to increase significantly in India.

As of now, India exports

around 70% of its production of 3 lac-3.5 lac MT. Karnataka accounts for 85% of

Indian production while the rest comes from Kerala. So with rising

consumption in India, India has sufficient local production to cater to the

demand. And now the trend is clearly towards coffee consumption in India and

this will grow much faster than tea. In fact I feel we may see coffee

plantations growing up in India even in the Himalayas where the black pepper

plantations may bend towards coffee. So i think slowly more and more Indians

are moving towards coffee. I like it when in movies and TV Shows they show

actors holding a large coffee mug (though may be empty) because this is subtle

marketing and it hits the cords more effectively...though i am not sure whether

it is deliberate or not but if it is not then i think coffee marketing companies

should think over this seriously.

3 Coffee beans (though Coffee

beans are not really “beans” but seeds of the fruit of the coffee tree) are

just like any other agriculture commodity with limited pricing power but when

we move up the value chain the dynamics of this industry changes to one with

premium pricing power with premium brands like that of Starbucks or Cafe Coffee

Day (CCD). So the value proposition changes relevant to the type of producer

like a plantation company is prone to boom and bust cycles of all commodities

and Coffee is not an exception. Right now, coffee industry is witnessing bust

cycle and prices are trending lower.

In last 10 years or so, the cost

of inputs for coffee production has increased by some 250% however the prices

have been increased only by 175% so there is a clear over supply of coffee

beans in the global market. But coffee production is not that easy to start and

stop. Unlike other commercial crops like Wheat/rice where crops are planted

every year the plantations like Tea, Coffee etc. take much longer time to start

producing and in the subsequent years it is not beneficial to stop production

as massive investments have been made in the initial unproductive years.

It takes four to five years for a

coffee tree to start producing coffee fruits, while the land on which it grows

will produce fruit for about 25 years. Hence apart from routine inputs in the

form of fertilizers maximum annual costs are in the form of labour only.

The likes of Starbucks and

other retail chains brought a revolution in coffee drinking habits of the

people and this spurred the demand for coffee across the globe especially in

Europe and USA and more and more farmers started cultivating coffee as prices

were at life time highs. This started in Mid 90’s and culminated around 2007-08

and since then global supply has outpaced demand by fair margin putting

pressure on the prices.

In the last 4-5 years, Brazil and

Vietnam are producing more and more coffee even when international coffee beans

prices are lower. In fact, in dollar terms the cost of producing beans is

higher than the prices but still the poor farmers of Brazil and Vietnam are

being able to support even with these lower prices is only due to the fall in

currencies of these countries to Dollar. Fall in currency has enabled these

farmers to earn something more than their cost of production. However, Brazil

is mainly responsible for this supply glut in the global markets.

As Brazil produces massive 35% of

the global production (25% of global export market), so it is the main force

behind the rise and fall of global coffee prices. No other country has this

much power in controlling the coffee prices. Here, Brazilian currency Real has

major impact because Real is falling as compared to USD every day and this is

making Brazil coffee suppliers to sell more and more coffee even at lower

prices in Dollar terms because they are getting more Real for every ton of

coffee sold in international markets. The exchange rate of USD to Real was 1.68

Reals in 2011 but the same now is 5.3 reals!!! More than 3 times fall. The weak

real is putting more pressure on the global coffee prices.

4) So even when coffee prices are

ruling at 13 year ($1 per pound) low Brazil farmers were still able to extract

something but the situation is grim across the world for coffee producers.

Coffee producers across the globe are abandoning their coffee farms or turning

to other crops like Cocoa in Colombia which is the supplier of world’s best

quality coffees. So sooner or later coffee production is going to come down and

this will raise the prices to more reasonable levels.

But I feel there is another

crisis which may come with current situation. The countries where coffee

farmers are abandoning their farms are some of the best quality coffee

producers like Colombia, Guatemala, Kenya which means this will reduce the

supply of premium quality Arabica coffee and this may result in very high

prices for premium coffees and very low prices for Robusta coffees.

But still, even now people can

create the demand for premium quality coffee as prices are low. Low quality

coffee does not make people to consume more coffee but a cup of premium Arabica

coffee can make people to consume 3 cups in place of 1 cup of coffee and this

may create or raise the demand for premium coffee which is not within our reach

mainly because of low quality instant coffee used by most people so far. They

are no aware of the fine taste of a premium coffee.

Amid all this mayhem in global

markets, India is facing shortfall in its coffee production due to pest

attacks, climate issues. But this year is going to be good for Indian coffee

production and production will be higher. Also, Global coffee beans prices has

firmed up recently due to harvesting and supply chain issues faced by farmers

across the globe due to covid restrictions. So I think we may be near the end

of bust cycle of coffee and prices may start firming up from now on as supply

is going to shrink especially for premium Arabica coffee the prices may go up

much higher. So this year should be good for Indian Coffee plantation industry

including Tata Coffee Ltd.

5) But things are different for instant

coffee or retail coffee chain branded players like Nestle, Bru or Starbucks. As

for these retailers, the low prices of coffee beans are good as the prices of

their end product are driven by suppliers not by consumers as demand is stable

at current price. This is because they are not selling a homogenous commodity

but a branded product with distinct attributes, quality and taste so producers

are price settlers.

Tata coffee

Ltd: Indian Coffee story

Tata coffee is India’s largest

coffee producer. Indian coffee production is mainly about small farmers holding

small land holdings and instances of large corporate producers like Tata coffee

are very few. Tata coffee deals in coffee in all combinations- it has

plantation business producing raw coffee beans, it has instant coffee

production capacities, It has retail presence in USA through Eight O’ clock

coffee brand, sells instant coffee in India under “Tata coffee Grand” band, it

supplies roasted coffee beans to all Starbucks chains in India, it has also

developed Indian coffee blend for Starbucks chains across the globe.

Tata coffee owns around 8000

hectares (around 20000 acre) of Coffee plantations in southern India. If we

take Rs. 4-5 lac price per acre then the valuation of these coffee plantations

will be around 800-1000 cr. However, normally prices for Coffee estates are in

the range of Rs. 10 lac to Rs. 20 lac per acre especially in tourism heavy

areas like Coorg where Tata coffee owns around 11000 acres and this will make

the valuations anywhere near 2000 cr to 3000 cr!!! And we are still left with

2400 hectares (6000 acres) of tea estates. Recently Tata Coffee was looking to

acquire 12000 hectares of coffee plantations owned by troubled Café Coffee Day

for Rs. 1200-1500 cr (while CCD is asking for some 2000 cr) which supports our

calculation of minimum 1000 cr value for coffee plantations. Tata coffee has

entered into partnership with group hospitality company Indian Hotels for

managing its coffee heritage resorts for hospitality business. This also have

the potential for a good business going forward and this will further establish

the valuation of its coffee plantations.

Its recent expansion (invested

some 400 cr for new Instant coffee plant) in Vietnam has started performing

this year and mainly due to operation of its Vietnam plant its PAT for the first half is Rs. 59 cr vs 47

cr even during covid crisis which is an indication towards things to come in

the near future.

Merger with

Tata Consumer to unlock big Value and Synergy for Both

Tata coffee has 50.08% holding in

Eight O'Clock Coffee (ECL) which is a famous American retail coffee brand (Arabica

roast and ground coffee) dates back to 1859. Before Vietnam plant, ECL was

accounting for 60% of the total turnover- 1120 cr out of 1966 cr in 2019-20. ECL’s

net profit in 2019-20 was 117 cr but due to its 50% share only 58 cr accrue to

Tata coffee. But after Vietnam plant, NP will grow much faster as the same is

100% subsidiary of TCL. Its NP for the first half this year is 59 cr and I

think the same may touch 150 cr this year.

CCL Products India Ltd. (Market

value 3200 cr, PE 20) is another listed coffee player but it is more of a

wholesale producing instant coffee and does not own plantations but still its

valuation is same as of TCL. But I think both can’t be compared- Tata coffee

also has large Instant coffee business but it has much higher brand strength in

both B2B and B2C. In B2C it has a great brand in Eight O’clock coffee which is

growing fast in USA now so it should be valued as an FMCG brand. In 2006, Tatas

paid $ 220m (Rs. 1000 cr as per 2006 exchange rates and 1600 cr as per current

exchange rates for ECL acquisition. Tata coffee contributed 50% of the amount

($110m). At that time, ECL was having revenues of $110m and the same right now

is around $160m so as we can see not that much high growth by ECL. And this may

be one of the reasons for the underperformance of Tata coffee because biggest

revenue contributor was not growing that much. But ECL once was top coffee

brand in USA and Tatas are now working on revamping the brand and supply chain

and this should show the impact pretty soon.

I have not done its valuation

exercise comprehensively but 50% stake should value around 1500 cr Rs. (at 20-25

PE). 1500 cr value for 50% stake in ECL is still at the lower end as it would

make for just 2 times returns for Tata coffee in ECL in last 14 years. US is

still and will be the biggest coffee market globally (70% consumption at home

which augurs well for ECL) and that’s why ECL is critical to Tata group and

they are restructuring its business in USA and this year the growth is good in

ECL and looks like the strategy is working. Total Income of Eight O'Clock

Coffee Company for the Six months ended September 30, 2020 was USD 87 .81

Million compared to USD 76.48 Million for the corresponding Six months of the

previous year. Further, I think as demand for

premium coffee will rise in India for home consumption there is a possibility

that Tata may introduce ECL in Indian market. And I feel Tata should make the

first move rather than waiting for other brands like Nestle. Recently, many

brands have started offering premium coffee beans in India for home consumption

like Blue Tokai which are witnessing high demand. Though Tata Coffee has also

introduced their single estate coffee brand “Sonnet” but still I feel ECL is an

established brand and have time tasted blends for USA market and these blends

should do well in India markets with some tweaking for Indian tastes (though I

think there is nothing like Indian taste in Indian coffee as of now). ECL can

benefit from vast supply chain and distribution reach of Tata consumer which is

way bigger than ECL in USA.

Balance

50% holding in ECL is with Tata consumer which is also the holding company of

Tata coffee (57% holding) and that’s why I feel Tata coffee may be merged with

Tata consumer and at that time there will be value unlocking for plantations of

more than 25000 acre (coffee and Tea) which are not valued much in the current

valuation but for merger they should get the valuation of around 1000 cr.

Tata consumer is already doing

the distribution and marketing for “Tata coffee Grand” brand owned by Tata coffee

Ltd. Tata group is on a great value accretive restructuring path simplifying

ownership, supply chain and management structure and there is no reason for

Tata consumer to leave Tata coffee alone when they have already restructured

the FMCG brands of Tata chemicals.

Tata

Starbucks- Emerging Giant of Indian retail coffee

Tata coffee is the exclusive

supplier of coffee beans to Tata-Starbucks (50:50 JV) in India and has also

started supplying the same for their global business and this is going to make

a mark for Indian coffee blends in the global market just like Indian single

malt whiskies by Amrut/Paul John/Rampur. Tata Coffee has revamped its

plantations into 8000 micro grids to cater to the premium beans requirements of

Starbucks. Growth of Starbucks in India means growth for Tata coffee. It is for the first time in the history of Starbucks that

they are procuring coffee from the roasting facility owned by its partner. This

shows the expertise of Tata coffee in producing premium quality coffee. This

localization also saves the costs for Tata-Starbucks as they are not required

to import costly coffee. Coffee drinking in India is moving beyond south Indian

states and coffee retail brands are going to see big growth in the future and

Starbucks should be the leader of the pack. Tata-Starbucks turnover last year

was 540 cr and it is already profitable and Starbucks is very aggressive about

Indian market growth.

Indian coffee market is still in

its infancy just like China. Just like India, China was a country of tea

drinkers. But Starbucks happened to china in 1999. Starbucks has succeeded in

blending coffee culture into Chinese culture and it has done the same by

relentless attention on details in creating Starbucks a place where Chinese

people love to enjoy best coffee, sit, relax and enjoy with their friends.

Starbucks has focused on integrating local customs and designs in its cafes. Starbucks

were aware of the growing middle class in China and its powerful impact on

demand and need for new recreational places. Coffee is a western drink but young

Chinese considers coffee culture sophisticated and to influence. It is normal

for people in China these days to have business meetings and even job

interviews at Starbucks. So with great execution, Starbucks has been successful

in creating its cafes as place to go after home and office. The same thing

happened in Japan which was another tea drinking nation and now a big coffee

nation with Starbucks having more than 1000 stores. Starbucks is having some 4400

stores in China, the largest outside USA and it is betting big on China as next

big market after USA. Its China revenues are around 6000-7000 cr which are only

going to grow bigger in the next 2-3 years as Starbucks is looking to double

the store count.

So India is going to follow the

footsteps of Japan and China in adopting the coffee culture and Tata coffee as

a supplier of premium coffee beans will be one of the major beneficiary of this

shift. Starbucks has worked out a great marketing strategy for Chinese market

and developed and created products keeping in view the Chinese tastes. Chinese

are much more serious about their culture and family value and social status.

So Starbucks did some great marketing there- No aggressive Coffee promotions to

avoid being treated as a threat to their tea-culture, blended Coffee culture

with tea culture initially, engaging annual family programs etc. Starbucks is a

giant success in creating great and innovative coffee products and it is doing

this for decades. Starbucks had partnered with local partners for China market

in order to address the complexity of massive china market. The same thing it

has done for Indian market which is going to as massive as China and after a

lot of search it partnered with India’s most trusted and iconic brand Tata. The

selection of Tata itself shows the brand strength, trust and customer loyalty

it has in Indian market. If you ask any Value investor- China was not a market

where Starbucks could achieve any sort of success but with their superior

executing skills they have made it their biggest outside USA and may one day

even bigger than USA. So I have no doubts that they will do the same in Indian

market also.

As of now, Tata-Starbucks operates

200 stores in India across 13 cities. Tata’s stake is owned by Tata consumer

product ltd (TCPL) and as of now they have invested around 300 cr in the JV.

But if you ask me the creation of

a coffee culture by Starbucks in India will have multi-dimensional impact on

coffee demand in India not just for retail chains of Starbucks but also for

home consumption and Tata coffee is going to be the major beneficiary here also

as it is focusing on developing premium Coffee products for Indian markets.

Recently it has launched premium single estate retail coffee brand “Sonnet”

which is available online.

Tata Coffee being an integrated

coffee player is going to be a major beneficiary of coffee industry growth in

India as it can restructure its product offerings as per the requirements of

the market like it can shift the export of its premium quality coffee beans to

meet the higher demand of Starbucks outlets in the future. For any premium

coffee retail brand like Starbucks the supply of uniform premium quality beans

is the foremost requirement and Tata coffee can maintain this supply through

premium coffee produced in its coffee plantations.

Troubled Cafe

Coffee day- An opportunity for Tatas to acquire assets and Relative strength

Troubled Cafe Coffee Day

enterprise is looking to sell various assets/businesses to pay off the debt.

Promoter family is also selling their assets to reduce the debt at promoter

level. Tatas are interested in their Coffee plantations spanning 12000 hectares

and Coffee vending machine business. Talks were at advanced stage and are

taking time due to issues related to valuations and some creditors asking for

more. I think we will see something on this very soon... may be within a month

or so. Tata coffee and Tata consumer will do anything to acquire these assets.

The acquisition of coffee plantations will make Tata coffee a substantial

player in Indian coffee beans market and it will be an integrated coffee

player- all the way from plantations to retail sale and coffee chains.

Some

analyst friends have questioned this asset heavy approach but I think owned

plantations are a key to ensure and control the coffee bean quality and Tata

coffee is eyeing premium-ness in its products now. India is going to witness a

coffee culture at home and out of home and this will create massive demand for

quality coffee beans and that’s why having its own plantations will ensure the

supply without any worry of the beans prices. Now, Tata coffee wants to be

established as a premium brand. Brand strength and loyalty in B2B is more

strong and relationships like supplier of Starbucks are tough to create and are

long lasting (Just check the valuation of recent IPO of Mrs Bectors).

Tata coffee was in restructuring

mode for last 5-6 years and the stock has not performed at all during this

period. It is still available at 2014 valuations. So it has gone nowhere. I

think as of now, market has valued it as some sort of plantation company but

the share of plantation business and its impact on NP has come down to great

extent in the last 4-5 years and now it is more of coffee product company so

its re-rating catalyst are just nearing now and it may get the re-rating quite

fast just like the same has happened in many tata group stocks- Tata consumer, Tata

Motors, Tata communications, Tata chemicals and Tata power (we hold all).

I think things are nicely shaped

for Tata coffee to witness a high growth phase and at a valuation of 2000 cr I

think market is not valuing its various businesses adequately.

Summary of Analysis levels Involved in the

study of Tata coffee:

1.

Level 1 (Lower relative valuation) -

Current stock price is not reflecting the value of its coffee and tea

plantations, value of its overseas subsidiary Eight O’clock Coffee.

2.

Level 2 ( Industry level growth and restructuring)- Tata coffee is

going to see massive growth in its premium coffee beans and instant coffee

business due to growth of coffee demand in India both for home consumption and

Coffee retail chains.

3.

Level 3 (Forecasting of management decisions which may result in massive future

growth and value unlocking) - (a) Merger of Tata coffee with Tata consumer products

Ltd (b) Acquisition of Coffee plantation assets of CCD.

(This study is a business analysis of Tata Coffee Ltd. Views are personal and should not be taken as a recommendation for buying or selling a stock. Stock markets are inherently risky so kindly do your own Due Diligence before investing. I am not a certified Sebi Analyst and holding the shares discussed in this Post. This business study of Tata coffee Ltd is taken from the Monthly Newsletter (Jan-21 Edition) of this Blog. For subscribing to the monthly Newsletter reach at oscillationss@yahoo.in).